Messaging And Report Category: Fact Sheet

Why Fair Housing, Fair Lending and Equal Opportunity

The meltdown of the home mortgage market, the scourge of foreclosures, and the decimation of family and community assets that have ravaged the U.S. economy affect virtually every American and our nation as a whole. At the same time, communities of color have been especially hard hit by the crisis, in uniquely damaging ways that are potentially long lasting. This fact sheet documents the role that discrimination and unequal opportunity have played in the home opportunity crisis, as well as some of the harm that those practices have caused to our nation.

Key findings include:

- A longstanding pattern by lenders and brokers of targeting communities of color for risky, high-cost loans, controlling for other factors such as credit history—with higher income families of color receiving the most unequal treatment.

- Racial discrimination in the terms and conditions of loans by some of the nation’s largest banks.

- Unequal maintenance of foreclosed properties, with banks and others disproportionately neglecting properties in communities of color.

- Failure of governmental bodies, including the Departments of Treasury and Housing and Urban Development and the Federal Housing Finance Agency, to adopt or adequately enforce fair housing and lending protections.

Homeownership has long been an important steppingstone to the middle class for African Americans, Asian Americans, and Latinos, and the crisis struck at a time when access to homeownership had only recently opened up to these families on a significant scale. As politicians removed banking and consumer protections and neglected fair housing and lending enforcement, unscrupulous lenders and brokers targeted communities of color for risky subprime loans with high rates, exorbitant fees, and frequently deceptive terms. The racial targeting was made easier by America’s legacy of residential segregation, and by the relative lack of traditional banks in many communities of color. Millions of black and Latino homeowners—many of whom qualified for standard 30-year fixed mortgages—were marketed subprime loans that were destined to fail. Indeed, higher income African Americans were especially likely to receive risky loans, as compared with similarly qualified white homeowners.

Not surprisingly, then, families and communities of color have been especially hard hit by the fallout of the home opportunity crisis, in terms of lost homes and dislocation, diminished assets and credit, and neighborhoods dotted with foreclosed and shuttered properties. Some experts have predicted that the economic crisis will represent the greatest loss of wealth to the black community since the end of Reconstruction.

Conversely, effective and inclusive solutions to the crisis are especially important to the progress and equal opportunity of communities of color, as well as to the nation as a whole. This requires both general approaches that prevent foreclosures and restore communities across the board, as well as equal opportunity and civil rights approaches that target the particular harm that discriminatory practices and violations of fair housing and lending laws continue to cause in communities of color.

Housing, consumer protection, economic, and civil rights experts have assembled the most promising of those solutions in a Compact for Home Opportunity. The Compact is part of the Home for Good campaign, which calls for adopting the concrete, effective, and inclusive remedies that are needed to promote greater and more equal home opportunity for all.

What follow are the specifics of the impact of the home opportunity crisis on people of color.

Targeting of Communities of Color for Risky, High-Cost Loans

Housing discrimination, residential segregation, and unfair lending practices against people of color were long a feature of the U.S. home opportunity landscape. Civil rights laws like the Fair Housing Act and Equal Credit Opportunity Act have helped to reduce those practices, but have not eliminated them. These discriminatory patterns served as the foundation for unequal home opportunity in the current era.

During the 1990s, the rise of subprime lending and mortgage securitization created the tools and incentives that led subprime specialists to target communities previously denied access to conventional credit—especially African-American and Latino communities and families. Unscrupulous lenders sold these high-cost loans, which were originally intended as a temporary credit accommodation, to people who qualified for prime loans, and also to borrowers with weak credit who could not afford the loans.1 Lenders intensified these unethical practices in response to increasing demand from financial firms that bundled subprime mortgages into securities products.2

Over time, a “dual mortgage market” developed, in which different racial and ethnic communities were offered “a different mix of products and by different types of lenders,” and subprime lenders “disproportionately target[ed] minority, especially African American, borrowers and communities, resulting in a noticeable lack of prime loans among even the highest-income minority borrowers.”3 A large body of research documents these policies. For example:

- In a 2006 report using federal data, The Opportunity Agenda, the National Community Reinvestment Coalition, and the Poverty and Race Research Action Council warned that— even controlling for income—African-American and Latino borrowers were significantly more likely to be sold high-cost, subprime loans than whites, despite the fact that as many as 50% of those borrowers qualified for prime loans. Racial inequity in lending actually increased with borrower income levels, and with the degree of neighborhood segregation. Loans in these communities were more costly, and were frequently predatory, carrying hidden fees and conditions or marketed through deceptive practices. Some, for example, were designed with built-in rate adjustment features making them unsustainable over the loan’s lifespan.4

- One study found that, within the subprime market, “borrowers of color . . . were more than 30 percent more likely to receive a higher-rate loan than white borrowers, even after accounting for differences in risk.”5

- Another study found that African Americans and Latinos were much more likely to receive subprime loans, and that “the disparities were especially pronounced for borrowers with higher credit scores.” (emphasis added)6

- Researchers at Princeton University studied the links between neighborhood racial composition, subprime lending, and foreclosure rates, and found “strong empirical support for the hypothesis that residential segregation constitutes an important contributing cause of the current foreclosure crisis, that segregation’s effect is independent of other economic causes of the crisis, and that segregation’s explanatory power exceeds that of other factors hitherto identified as key causes (e.g., overbuilding, excessive subprime lending, housing price inflation, and lenders’ failure to adequately evaluate borrowers’ creditworthiness). Simply put, the greater the degree of Hispanic and especially black segregation a metropolitan area exhibits, the higher the number and rate of foreclosures it experiences.”7

Racial Discrimination in Terms and Conditions of Loans

In addition to targeting minority communities for risky subprime loans, many big and small institutions within the lending industry also discriminated against communities of color in the terms, conditions, and cost of the loans they did offer.

- U.S. Department of Justice discrimination settlement with Wells Fargo Bank. In July 2012, the Department of Justice filed the second largest fair lending settlement in the its history to resolve allegations that Wells Fargo Bank, the largest residential home mortgage originator in the United States, engaged in a pattern or practice of discrimination against qualified African-American and Hispanic borrowers in its mortgage lending from 2004 through 2009. The settlement provides $125 million in compensation for wholesale borrowers who were steered into subprime mortgages or who paid higher fees and rates than white borrowers because of their race or national origin. The Justice Department’s complaint contends that Wells Fargo discriminated by steering approximately 4,000 African-American and Hispanic wholesale borrowers, as well as additional retail borrowers, into subprime mortgages when non-Hispanic white borrowers with similar credit profiles received prime loans. All the borrowers who were allegedly discriminated against qualified for Wells Fargo mortgage loans according to Well Fargo’s own underwriting criteria. The Justice Department further claimed that, between 2004 and 2009, Wells Fargo discriminated by charging approximately 30,000 African-American and Hispanic wholesale borrowers higher fees and rates than non-Hispanic white borrowers because of their race or national origin rather than the borrowers’ credit worthiness or other objective criteria related to borrower risk.8

- U.S. Department of Justice $335 billion discrimination settlement with Countrywide Financial. In December 2011, the U.S. Department of Justice (DOJ) reached the largest fair lending settlement in its history with Countrywide Financial. The settlement resulted from a lawsuit in which DOJ alleged that Countrywide had discriminated on the basis of race and national origin against qualified African American and Hispanic borrowers between 2004 and 2008. The lawsuit alleged that Countrywide charged more than 200,000 African- American and Hispanic borrowers higher fees and interest rates than non-Hispanic white borrowers, and steered borrowers of color into subprime loans. The data indicated that these disparities were not due to borrowers’ creditworthiness or other objective criteria related to borrower risk.9

- U.S. Department of Justice settlement with AIG subsidiaries. In March 2010, the U.S. Department of Justice settled a case against AIG Federal Savings Bank (FSB) and Wilmington Finance Inc. (WFI), two subsidiaries of American International Group, Inc., in which the Justice Department said the banks engaged in a pattern or practice of discrimination against African-American borrowers in violation of the Fair Housing Act and the Equal Credit Opportunity Act. DOJ alleged that the defendants charged higher fees to thousands of African-American borrowers nationwide between 2003 and 2006, and failed to supervise or monitor brokers in setting broker fees. The settlement terms required the defendants to pay $6.1 million to African-American customers who were charged higher broker fees than non-Hispanic white customers; required the defendants to invest at least $1 million in consumer financial education efforts; and prohibited the defendants from discriminating on the basis of race or color in any aspect of wholesale home mortgage lending.10

- U.S. Department of Justice settlement with PrimeLending. In January 2011, the Justice Department announced a settlement resolving allegations that PrimeLending discriminated against African-American borrowers nationwide between 2006 and 2009 by charging African-American borrowers higher annual interest rates than it charged similarly situated white borrowers, including in loans guaranteed by the Federal Housing Administration and Department of Veterans Affairs. The terms of the settlement required PrimeLending to pay $2 million to borrowers identified as victims of discrimination, as well as to engage in loan pricing policies, monitoring and employee training designed to prevent future discrimination.11

- U.S. Department of Justice settlement with C&F Mortgage Corporation. In September 2011, the Justice Department reached a settlement with C&F Mortgage Corporation, resolving allegations that the C&F had violated the Fair Housing Act and the Equal Credit Opportunity Act by charging higher interest rates (in the form of “overages”) and giving lesser discounts on mortgage loans to African-American and Hispanic borrowers. The consent decree required C&F to develop uniform policies for all aspects of its loan pricing and to phase out overages, as well as to pay $140,000 to black and Hispanic victims of discrimination, monitor loans for disparities based on race or national origin, and provide antidiscrimination training for employees.12

- U.S. Department of Justice settlement with Midwest BankCentre. In June 2011, the Justice Department reached a settlement with Midwest BankCentre, which it said provided unequal home mortgage lending services to residents of majority African American neighborhoods, as compared to residents of predominantly white neighborhoods (in other words, that it was “redlining” the minority neighborhoods). These allegations focused on the Bank’s practices in the St. Louis metropolitan area. Midwest BankCentre agreed to open a full-service branch in an African-American neighborhood, and to invest in the formerly redlined majority areas through a special financing program extending credit to those areas, as well as spending $300,000 for consumer education and credit repair programs, and $250,000 for outreach to potential customers.13

- U.S. Department of Justice settlement with Citizens Republic Bancorp. In June 2011, the Justice Department entered into a settlement with Citizens Republic Bancorp, Inc., which it alleged had violated the Fair Housing Act and the Equal Credit Opportunity Act by failing to provide mortgage lending services to the residents of majority African-American neighborhoods, as compared to residents of predominantly white neighborhoods (“redlining”). The allegations examined Citizens Republic’s lending services in the Detroit metropolitan area. Under the terms of the settlement agreement, the defendants were required to open and operate a lending office in an African-American neighborhood, and to invest in the formerly redlined areas of Wayne County through a $1.5 million financing program designed to increase the credit the bank extends in those areas. The bank also agreed to partner with the City of Detroit to provide $1.625 million in matching grants for existing homeowners to make exterior improvements, and to spend $500,000 for targeted outreach and consumer education.14

- U.S. Department of Housing and Urban Development and Housing Authority of Baltimore City settlement with public housing residents. In a long-running legal battle over fair housing options in Baltimore, in August 2012, HUD and the city of Baltimore’s housing department filed a proposed settlement agreement of a class action in Thompson vs. HUD,15 brought by African-American residents of public housing in Baltimore. In 2005, a federal judge held that HUD violated the Fair Housing Act by concentrating public housing in the most impoverished, segregated areas of Baltimore. The conditions of the agreement included the continuation of the Baltimore Housing Mobility Program, which voluntarily places public housing tenants throughout the city or in the suburbs. Started in 2003, the program has assisted more than 1,800 families move to new areas. In November 2012, a U.S. District Court judge approved the proposed settlement agreement. Key elements of the approved settlement include, among other things, continuing the mobility program, which provides Housing Choice vouchers and counseling, for up to 2,600 additional families through 2018; and requiring HUD, for a period of at least three years, to conduct civil rights reviews of specific plans and other proposals submitted to HUD for approval, involving certain federally funded housing and community development programs in the Baltimore region.16

- Pending litigation in Beverly Adkins et al. v. Morgan Stanley. On October 15, 2012, the ACLU, the National Consumer Law Center, and a San Francisco-based law firm brought a lawsuit on behalf of African-American homeowners in the Detroit area and Michigan Legal Services against the investment bank (as opposed to the subprime lender) for adopting mortgage securitization policies that caused predatory lending targeted at black homeowners. This is the first lawsuit that seeks to connect racial discrimination to the securitization of mortgage-backed securities.17

- Pending litigation in National Fair Housing Alliance (NFHA) v. Bank of America. On October 23, 2012, NFHA filed a federal housing discrimination complaint with HUD against Bank of America resulting from an undercover investigation that found that the bank maintains and markets foreclosed homes in white neighborhoods in a much better manner than in African-American and Latino neighborhoods in Chicago, Milwaukee and Indianapolis.18

Unequal Maintenance of Foreclosed Properties

Discriminatory treatment continues even after foreclosure. A detailed undercover investigation by the National Fair Housing Alliance and several regional partners found not only that banks too frequently fail to maintain foreclosed properties that they own, but that they tend to neglect their properties in communities of color at a much higher rate, with devastating consequences. A large number of the neglected, bank-owned properties have broken or missing doors and windows, inviting vandalism and trespassers. And many have safety hazards that endanger the public. Those and other defects are significantly more prevalent in bank-owned properties located in communities of color. Another finding is that, on average, the banks are not marketing houses located in communities of color as aggressively to individual homebuyers as they do properties in white neighborhoods. The properties in white neighborhoods are, for example, more likely to have clear and professional “for sale” signs. When banks both poorly maintain and market foreclosed houses, the properties tend to stay vacant longer and to eventually be sold to speculators, rather than to people who would make the houses their home.19

Governmental Failure to Adopt or Enforce Fair Housing and Lending Protections

The lack of adequate fair housing and lending rules and enforcement was a significant contributor to the foreclosure crisis and its unequal impact. This neglect was particularly egregious during the Bush Administration, but some troubling patterns continue today.

- Almost 50 years after the adoption of the Civil Rights Act of 1964, the Treasury Department is one of the only governmental entities that have not adopted regulations to enforce the Act.

- While the U.S. Department of Housing and Urban Development finalized in February 2013 important regulations relating to “disparate impact” discrimination (i.e., policies that are unnecessarily discriminatory in their effect, though not their intent),20 the agency still has not issued regulations implementing its duty to affirmatively further fair housing.

- In 2008, the bi-partisan National Commission on Fair Housing and Equal Opportunity found, among other things:21

- “[T]hat despite strong legislation, past and ongoing discriminatory practices in the nation’s housing and lending markets continue to produce levels of residential segregation that result in significant disparities between minority and nonminority households, in access to good jobs, quality education, homeownership attainment and asset accumulation.”

- “More than four million instances of housing discrimination occur annually in the United States and yet fewer than 30,000 complaints are filed every year. In 2007, the 10 HUD offices processed 2,440 complaints, the 105 [Fair Housing Assistance Program] agencies processed 7,700 inquiries, and the 81 private fair housing agencies processed 18,000 complaints. Literally millions of acts of rental, sales, lending, and insurance discrimination, racial and sexual harassment discrimination, and zoning and land use discrimination go virtually unchecked.”

- Delays in the administrative processing of cases [by HUD] have been so severe that they have served as the basis for dismissal of cases by courts and administrative law judges.

- “[The Government Accounting Office] found that only 16 percent of complainants who were identified as having potential cases were assisted with filing complaints. Even worse, 30 percent of callers who attempted to file a complaint could not get through on their first try, and some callers did not receive a call back even after three tries. Finally, when complaints were filed, only half were filed within 20 days from the initial date of contact with the agency. This kind of delay results in lost housing opportunities, missed opportunities to conduct testing, and loss of credibility about the agency’s functions.

The Result: Disproportionate Foreclosures and Loss of Assets

The combination of misconduct by banks and brokers, inadequate rules and enforcement, and record long-term unemployment have devastated the home opportunity and assets of millions of Americans, with communities of color shouldering a disproportionate and devastating burden.

- Homeowners and communities of color have been especially hard hit by foreclosures. For mortgages originated between 2004 and 2008, 5.1% of non-Hispanic white borrowers lost their homes to foreclosure, compared to 9.8% of Blacks/African Americans and 11.9% of Hispanics/Latinos, and 6.6 percent of Asian Americans. (During the same period, while low- and moderate-income Asian-American borrowers had a lower foreclosure rate than lower-income non-Hispanic whites, the pattern is reversed among middle- and higher-income Asian Americans.)22

- In a 2011 study of the loss in home equity among Asian American–Pacific Islanders, between 2007 and 2009, the median property value of Asian-American homeowners decreased by $42,900 while the property value loss for Native Hawaiians and Pacific Islanders (NHPI) was $47,000, compared to the national equity loss of $9,100 during the same period. The study attributed much of the large differential in equity loss to the fact that Asian Americans and NHPIs were highly concentrated in geographic areas where the housing downturn was more severe than in the rest of the country, e.g., Los Angeles, Chicago, and New York.23

- One illustrative study looked at Prince George’s County, Maryland, the wealthiest African- American county in the nation, finding that the national foreclosure crisis has had a profound effect on it. Analyzing the likelihood of foreclosure in Prince George’s County, the study found that the borrowers in Black/African American neighborhoods with high-income were 42% more likely and Hispanic/Latino neighborhoods with high-income were 159% more likely than the borrowers in non-Hispanic white neighborhoods to go into foreclosure, controlling for key demographic, socioeconomic, and financial variables.24

- The Center for Responsible Lending predicts that “the spillover wealth lost to African- American and Latino communities between 2009 and 2012 as a result of depreciated property values alone will be $194 billion and $177 billion, respectively.” [“spillover” costs refers to financial and nonfinancial consequences for homeowners who live near foreclosed properties].25 In an October 2012 white paper published by the National Community Reinvestment Coalition which reviewed the literature on the long-term social impacts and financial costs of foreclosure on communities of color, the authors cited U.S. Census Bureau figures that as of the fourth quarter of 2011, the non-Hispanic White, Black/African- American, and Hispanic/Latino homeownership rates were at 73.7, 45.1 and 46.6 percent, respectively. These rates compared to those reported for the fourth quarter of 2007, when the recession officially began, reflecting homeownership rates at 74.9, 47.7, and 48.5 percent, respectively.26

- The Inspector General for the Federal Housing Finance Agency (FHFA)—the agency that controls Fannie Mae and Freddie Mac—found that the FHFA does not adequately oversee these enterprises’ compliance with consumer and civil rights protections in their dealings with entities (“counterparties”) that sell loans to or service them for the enterprises. The Office of the Inspector General (OIG) for FHFA declared “FHFA does not examine how the Enterprises monitor compliance with consumer protection laws, and, indeed, OIG determined that the Enterprises do not ensure that their counterparties’ business practices follow all federal and state laws and regulations designed to protect consumers from unlawful activities such as discrimination.”27

Solutions: The Compact for Home Opportunity

Concrete, pragmatic solutions exist that can address these discriminatory patterns and their aftermath while expanding opportunity and economic prosperity for all Americans and rebuilding our economy. In coalition with housing, consumer protection, economic, and civil rights experts, The Opportunity Agenda has assembled a Compact for Home Opportunity, containing over a dozen strategies designed to promote successful homeownership, fair housing and lending, and the restoration of community and family assets.

- Department of Housing and Urban Development and Department of the Treasury, Curbing Predatory Home Mortgage Lending (2000); Ira Goldstein with Dan Urevick-Ackelsberg, The Reinvestment Fund, Subprime Lending, Mortgage Foreclosures and Race: How Far Have We Come And How Far Have We To Go? (2008).

- See, e.g., KATHLEEN C. ENGEL AND PATRICIA A. MCCOY, The Subprime Virus: Reckless Credit, Regulatory Failure, and Next Steps 56-58 (2011).

- William C. Apgar, Jr. and Allegra Calder, The Dual Mortgage Market: The Persistence of Discrimination in Mortgage Lending, in THE GEOGRAPHY OF OPPORTUNITY: RACE AND HOUSING CHOICE IN METROPOLITAN AMERICA 102 (Xavier De Souza Briggs, ed., 2005). See also William C. Apgar, Jr., Christopher E. Herbert and Priti Mathur, Department of Housing and Urban Development, Risk or Race: An Assessment of Subprime Lending Patterns In Nine Metropolitan Areas (Aug. 2009).

- The report is available at opportunityagenda.org.

- Debbie Gruenstein Bocian, Keith S. Ernst and Wei Li, Center for Responsible Lending, Unfair Lending: the Effect of Race and Ethnicity on the Price of Subprime Mortgages 3 (May 31, 2006).

- Debbie Gruenstein Bocian, Wei Li, Carolina Reid, and Roberto G. Quercia, Center for Responsible Lending, Lost Ground, 2011: Disparities In Mortgage Lending and Foreclosures 5 (2011).

- Jacob S. Rugh and Douglas S. Massey, Racial Segregation and the American Foreclosure Crisis, 75 AM. SOC. REV. 629, 644 (2010).

- The consent decree, complaint, and Justice Department press release are available at justice.gov.

- The DOJ press release is available at justice.gov.

- The consent order is available at justice.gov.

- The complaint is available at justice.gov.

- The settlement agreement and complaint are available at justice.gov.

- The settlement agreement and complaint are available at justice.gov.

- The settlement agreement is available at justice.gov. The complaint is available at Settlement Agreement, Thompson v. HUD, No. MJG 95-309 (D. Md. filed August 24, 2012).

- Department of Housing and Urban Development, “Court Approves Final Settlement Thompson v. HUD,” press release, November 20, 2012.

- The ACLU press release and complaint are available at ACLU website.

- The NFHA press release is available at National Fair Housing website.

- National Fair Housing Alliance, The Banks Are Back – Our Neighborhoods Are Not: Discrimination in the Maintenance and Marketing of REO Properties, April 3, 2012.

- 78 Fed.Reg. 11460 (Feb. 15, 2013) and GPO website.

- Department of Housing and Urban Development, “HUD Issues Rule Formalizing Standard on Discriminatory Effects in Housing,” press release, February 8, 2013.

- Leadership Conference on Civil and Human Rights, The Future of Fair Housing (2008).

- Debbie Gruenstein Bocian, Wei Li, Carolina Reid, and Roberto G. Quercia, Center for Responsible Lending, Lost Ground, 2011: Disparities in Mortgage Lending and Foreclosures (2011).

- “AAPIs Experience Significant Loss of Home Equity,” AsianWeek.com, January 29, 2011.

- Katrin B. Anacker, James H. Carr, and Archana Pradhan, Analyzing Foreclosures Among High-Income Black/African American and Hispanic/Latino Borrowers in Prince George’s County, Maryland, 39 HOUSING AND SOCIETY Issue 1, 1–28 (2012).

- Debbie Gruenstein Bocian, Wei Li, and Keith S. Ernst, Center for Responsible Lending, Foreclosures by Race and Ethnicity: The Demographics of a Crisis 11 (June 18, 2010). See also James H. Carr, Katrin B. Anacker and Michelle L. Mulcahy, National Community Reinvestment Coalition, The Foreclosure Crisis and its Impact on Communities of Color: Research and Solutions 31 (Sept. 2011) (discussing the racial wealth gap).

- James H. Carr and Katrin B. Anacker, National Community Reinvestment Coalition, Long Term Social Impacts and Financial Costs of Foreclosure on Families and Communities of Color: A Review of the Literature 3 (Oct. 2012).

- Federal Housing Finance Agency Office of Inspector General, FHFA Should Develop and Implement a Risk- Based Plan to Monitor the Enterprises’ Oversight of Their Counterparties’ Compliance with Contractual Requirements Including Consumer Protection Laws 2, March 26, 2013.

Expanding Opportunity for All: Economic Justice

This memo provides guidance for discussing greater and more equitable job creation with policymakers, media, and persuadable members of the public. While public and political demand for job creation is high, public attitudes toward the role of government, the success of the Recovery Act, and the need for deficit reduction increasingly stand in the way of effective action on this front. And the importance of ensuring quality jobs that reach all of America’s diverse communities is often lost in the debate. This memo includes background information on the economy and employment, current public opinion research, and messaging advice about starting constructive discussions on job creation.

Putting America Back to Work

Creating good jobs that help American workers take care of their families is an urgent national priority and central to preserving the American Dream for all. We can’t just wait for jobs to happen; we need public investment in expanded job opportunities for everyone. Jobs need to be available at all levels of the economy, and in all sectors, and we all have a stake in making that happen. We’ve seen what happens when we ignore the fact that we’re all tied together in this economy. It’s time to implement policies that work for everyone.

The Impact of the Stimulus: Economic Assessments and Public Attitudes

Despite public questions about the efficacy of the stimulus, prominent economists have noted that, absent intervention, the economy would have worsened significantly.1 In fact, according to some estimates, without the stimulus, “GDP in 2010 would be about 11.5% lower, payroll employment would be less by some 8½ million jobs, and the nation would now be experiencing deflation.” 2

Such assessments are complicated by conflicting public opinions about government’s role in rescuing the economy. For example, Americans want the government to act, but lack faith in its ability. A post- stimulus survey3 found that more than 60 percent of respondents felt that the government needed to “take a larger and stronger role” in resolving the economic crisis. At the same time, “most individuals believe they personally got themselves through the recession rather than lawmakers”1 and are skeptical that the stimulus plan passed last year has really made much difference in putting us on the road to recovery (42 percent say it will not help improve the economy and 44 percent see no impact).4 This attitude may be fueled in part by fears about the impact of the stimulus on the deficit. When asked about the biggest issues that may face the country 25 years from now5, 14 percent indicated that the deficit will be the greatest concern, whereas 11 percent believe that it will be the economy in general. Americans believe that the current economic situation is dire and must be dealt with, but are also worried about the future effects of present-day intervention.

Mid-2010: The U.S. Economy and Employment Outlook

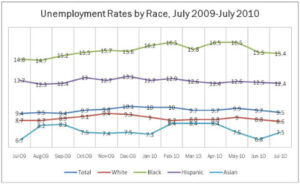

Despite minimal improvement in the unemployment rate (see Figure 1) due to the impact of the February 2009 stimulus package and other recovery efforts, not everyone is experiencing a positive trend. In fact, many groups who experienced unequal opportunity before the downturn face even more daunting challenges now. As Figure 1 shows, unemployment among African Americans and Latinos has remained 30 to 65 percent higher. Furthermore, month-by-month improvements in the total unemployment rate were not reflected by parallel gains in African-American employment.

Figure 1 Source – Economic Policy Institute’s Economy Track, www.economytrack.org/unemployment.php

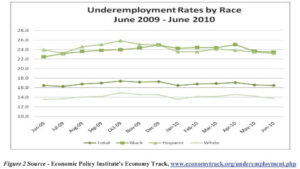

Underemployment rates, which track unemployed workers actively seeking work, involuntary part-time workers, and marginally attached workers, further highlight the depth and impact of the recent downturn. For example, while the underemployment rate for whites is lower than that of the total population, the African American and Latino/Latina rates – within a few points of each other, as seen in Figure 2 – are well above the rate for the total population.

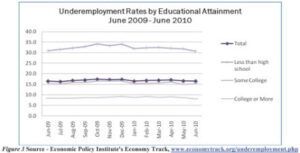

Even more startling is the difference in underemployment rates across educational levels. While the underemployment rate for those with some college closely mirrors that of the total population, a college or advanced degree ensures a notably lower underemployment rate. And those who have less than a high school degree have an underemployment rate that is double the rate of the total population (see Figure 3).

There were five unemployed workers for every current job opening6 at the end of June 2010. Further, due to population growth, even a “replacement rate” of jobs created would fail to ensure that the economy is “made whole.”7 Although, as of January 2010, 8.4 million jobs had been lost during the current recession, 11.1 million jobs would need to be created to return the country to a pre-recession unemployment rate.

While the gender pay gap hit a historic low of 82.8% in the second quarter of 2010, this is primarily due to the dramatic drop in male wages8. Unfortunately, this leveling in male-female pay disparities is headed in the wrong direction, representing lost income, when we need to improve and balance pay for everyone.

When discussing these economic realities, it is important to lay out for audiences why we should all care about them, and why, to restore the health of our economy, jobs and opportunity must reach all Americans.

Policies that focus only generally on job creation are likely to allow existing disparities to persist and, if not addressed, potentially worsen. An economic recovery that leaves whole groups behind like this is not sustainable and violates the core American values of opportunity and mobility for all. American principles of interconnectedness have real-world consequences for us all – a recovery that doesn’t include middle-class families lacks long-term stability. Furthermore, disparate rates of recovery hide serious problems for many.

Messaging Guidance

- Lead with values. Primary: Opportunity, Community/Common Good, Security. Secondary: Mobility, Redemption/Renewal, Voice, Accountability (use with care)

- Organize messages around a core narrative focused on The American Dream, Solutions, and the National Interest.

- Focus on jobs: Investment in quality jobs over immediate deficit reduction.

- Acknowledge progress on equal opportunity, while over-documenting barriers.

- Emphasize Government as a connector, planner, able to pave the way for progress.

- Tell thematic stories, connecting human stories to systemic problems and solutions.

- Frame the opposition’s approaches as divisive, impractical, and out of touch.

More Tips:

- Lead with values, such as the shared value of opportunity for all.

Those who want to work should have a chance to provide basic security and stability for themselves and their family. Good jobs are the foundation for realizing the American Dream for all. - Organize messages around a core narrative on economic recovery, including the themes: The American Dream, Workable Solutions, and National Interest.

The American Dream

This country stands for opportunity. We need to focus on expanding opportunity, not restricting it or allowing historic barriers to continue to foster inequality among us. The ability to care for one’s family, to move forward, and to thrive is at the core of the American Dream, and all of that depends on quality jobs. The American Dream must be available to everyone. Only a transformational, equitable recovery will ensure this treasured ideal continues to exist for all of us.

Workable Solutions

We have emerged from crises before by relying on American ingenuity and know-how, so it is within our power as a people not only to bring our economy back from this recession, but also to tackle the inequalities that burdened many communities before the downturn began. We need to move forward, with government paving the way, on a commonsense, practical agenda that expands opportunity for everyone here.

National Interest

The causes and effects of this economic crisis have illustrated how we are truly all in this together. When we allow inequality to fester and harm whole communities within our national fabric, it weakens us all. Recovery needs to be about mending and strengthening the entire cloth, so that we are prepared to face the future together.

- Focus on jobs: Investment in quality jobs over immediate deficit reduction.Economists agree that we must end the jobs crisis and the recession first. The best deficit reduction method is putting Americans back to work.

- Acknowledge progress on equal opportunity, while over-documenting barriers.Although the earnings gap between men and women has recently narrowed, it continues to affect us all. The current recession has resulted in more lost jobs for men, increasing the reliance of many families on women’s earnings. Currently, more than 12 million families with children rely primarily on women’s earnings.9 By eliminating the gender wage gap, those families would have access to 17- 23% more income, increasing the spending power and economic stability of these families, which is good for all of us.

- Emphasize Government as a connector, planner, able to pave the way for progress.Our nation’s greatest leaps forward have always come when we have invested in an effective partnership between government and our people. Think of child immunization programs that have wiped out devastating diseases in our country; our Social Security system that has enabled millions of seniors to move out of poverty, and Medicare, which has kept them safer and healthier regardless of their wealth, race, or ethnicity; even the interstate highway system, which connected us as a single prosperous nation. In order to effectively address this economic crisis, we need that kind of investment today.

- Tell thematic stories, connecting human stories to systemic problems and solutions.Those who want to work should be able to work. We’re all familiar with news stories showing people lined up around the block waiting to enter a job fair. This is only one example of the many people seeking opportunity, but encountering multiple barriers to it.

- Frame the opposition’s approaches as divisive, impractical, and out of touch.The suggestion that an unregulated market economy offers the best hope for creating opportunity ignores current economic realities. The worst economic downturn in decades was only reversed by unprecedented responses by monetary and fiscal policymakers.

Applying the Message

In order to deliver a consistent, well-framed message in a variety of settings, we recommend structuring opening messages in terms of Value, Problem, Solution, Action. Leading with this structure can make it easier to transition into more complex or difficult messages.

Value:

To preserve the American Dream for all, we need to ensure that everyone who wants and needs to work can do so.

Problem:

Unemployment rates have hovered near 10% for the past year, going as high as 16.5% for African Americans and 13.1% for Latinos/Latinas. However, public fears about the efficacy and cost of job creation have blocked investment in efficient, comprehensive, and equitable job programs.

Solution:

We must support public investment in job creation to prevent long-term damage from the downturn and reduce the future deficit by putting Americans back to work now.

Action:

Tell your representatives in Congress to support the restoration of the American Dream for all by voting for the Local Jobs for America Act.

Notes:

1. Lynch, D.J., Economists agree: Stimulus created nearly 3 million jobs, August 30, 2010.

2. Blinder, A.S., Zandi, M., How the Great Recession Was Brought to an End, July 27, 2010.

3. Gerstein/Agne at Demos/Topos Report.

4. Greenberg, S.B., Economic Mobility and the American Dream Survey, 2009, Greenberg Quinlan Rosner Research & Public Opinion Strategies.

5. Jones, J. M., Americans Say Jobs Top Problem Now, Deficit in Future, 2010, Gallup, Inc.

6. Job Openings and Labor Turnover Summary, August 11, 2010.

7. Turner, A. Jobs Crisis Fact Sheet, 2010, Economic Policy Institute.

8. Goudreau, J., Gender Wage Gap Shrinks To Record Low, September 14, 2010.

9. Boushey, H.; Arons, J.; Smith, L. Families Can’t Afford the Gender Wage Gap, 2010, Center for American Progress.

Ensuring Equal Opportunity in Our Nation’s Economic Recovery Efforts

When it comes to ensuring that the economic stimulus and recovery process promotes equal opportunity for all communities, the law is strong, but it is up to communities to uphold and enforce that law.

This fact sheet provides information and ideas for ensuring that federal investments in America’s economic recovery create greater and more equal opportunity for all. Specifically, it describes the ways in which existing laws require equal opportunity in jobs, housing, health care, transportation, and other sectors, and offers specific ideas for holding public and private officials accountable. This fact sheet is not intended to be legal advice, for which readers should consult an attorney.* Rather, it is intended to share information about public policy, and to stimulate action.

Federal laws protect equal opportunity and prohibit discrimination in virtually all of public and private efforts supported by the American Recovery and Reinvestment Act of 2009 (ARRA), also known as the “Recovery Act.” And the President has directed that agencies distributing those funds take proactive efforts to enforce them.

Who is “OMB” and what do they have to do with the “Stimulus”?

On February 13, 2009, Congress passed the Recovery Act. President Obama signed ARRA into law on February 17th. On February 18th, the White House Office of Management and Budget (OMB)—which assists the President with overseeing and supervising the Executive Agencies—issued a memo, known as the “Implementing Guidance,” that explained to all Executive Agencies the “requirements and responsibilities” in distributing the hundreds of billions of dollars in ARRA funds.

The Implementing Guidance describes procedures for distributing funds in great detail, including the requirement for agencies to ensure compliance of any government or private recipient of ARRA funds with equal opportunity, civil rights, fair labor, and environmental laws. On April 3rd, OMB updated the Implementing Guidance,1 clarifying the goals and requirements of ARRA. The update included a particular focus on the duty of agencies to comply with equal opportunity laws:

Federal agencies should take additional policy considerations into account, to the extent permitted by law and practicable […] such as supporting projects that ensure compliance with equal opportunity laws and principles [….]

(OMB Updated Implementing Guidance for the American Recovery and Reinvestment Act of 2009, April 3, 2009)

What is clear from the Implementing Guidance is that guaranteeing equal opportunity in the ARRA is both a goal of the White House and a legal responsibility of the agencies that are allocating the funds.

What are the Responsibilities of Federal Agencies Distributing Economic Stimulus Funds?

Equal opportunity is not just a good idea—it is the law. As stated specifically in the OMB Implementing Guidance, agencies distributing ARRA funds must:

- Ensure Compliance by ARRA Fund Recipients with All Anti-Discrimination and Equal Opportunity Statutes, Regulations, and Executive Orders including laws prohibiting discrimination based on race, ethnicity, national origin, sex, disability, and age2

- Ensure Preservation of the Environment through compliance with the National Environmental Policy Act,3 Endangered Species Act,4 and National Historic Preservation Act.5

- Guarantee Fair Wages by requiring contractors and subcontractors to pay no less than the “prevailing wages” found in a particular industry and metropolitan area, as required by the Davis- Bacon Act.6

What are the White House’s Policy Goals for the Economic Stimulus?

As explained in the OMB Implementing Guidance, the White House wants to implement the ARRA in a way that provides “long-term public benefits” and optimizes the economic activity and jobs created.7 To that end, all agencies are required to consider the following policy goals, to the extent possible given practical restraints, as they distribute ARRA funds:

- Compliance with Equal Opportunity Laws and Principles including laws requiring contractors receiving ARRA funds to guarantee that the economic opportunity created by these funds does not exclude persons or communities—either intentionally or in effect—on the basis of race, gender, age, disability, or national origin.8

- Long-term Public Benefits that improve Americans’ quality of life and economic efficiency, such as advances in technology, science, and health; environmental protection and infrastructure development; and educational quality improvements.9

- Optimizing Job Creation and Economic Activity in relation to dollars spent.10

- Transparency and Accountability in ensuring that projects are chosen using merit-based selection criteria, such as job creation, long-term benefits, and ability to deliver the results sought by the program.11

- Promoting Local Hiring and Community Engagement by supporting projects that provide job opportunities to those who live within the community where an investment is being made and that engage community-based organizations in connecting economic opportunities to those who have been historically excluded or overlooked.12

- Supporting Small Businesses by providing small businesses with the opportunity to compete for prime and sub-contract contracts, by utilizing existing agency offices for small disadvantaged businesses, and by awarding contracts to the extent allowed to disadvantage business enterprises.13

- Supporting Good Jobs by seeking to support contractors and subcontractors who have a proven record of complying with wage and hour, occupational safety and health, and collective bargaining laws.14

What Does “Equal Opportunity” Mean?

Creating equal opportunity—which is both a policy goal and requirement of ARRA—means that benefits and burdens resulting from ARRA projects should be distributed fairly and equally amongst the communities in which the projects are located.

Where a federally-funded project or program places fewer benefits or more burdens on a certain group of people based on race, gender, disability, national origin, or age, the result is a “discriminatory effect,” also known as a “disparate impact” because it creates a disparity. Title VI of the Civil Rights Act of 1964 and other equal opportunity laws forbid federally-funded programs and projects from having discriminatory effects or disparate impacts, and other laws prohibit such discrimination in both public and private employment, housing, and education, including job training.

Example: How an ARRA Project Should Be Implemented

To clarify the concept of preventing “discriminatory effects,” let’s consider a hypothetical transportation project, such as construction of a highway. The construction of a new highway connecting a city with inner and outer ring suburbs will entail state and federal (Department of Transportation) funding over multiple years. The project will include many positive opportunities for some communities, including job training, employment, contracting, and access to and from jobs, hospitals, schools, and shopping. There will also be short- and long-term burdens, including air and noise pollution, increased traffic, and the displacement of people from their homes and neighborhoods. In deciding whether to authorize the project, the Department of Transportation should consider the distribution of burdens and benefits such as:

- The demographics of the community affected as compared to those in the surrounding metropolitan area;

- Transportation needs of the community (as related to access to health services, centers of employment) and how those might be alleviated or worsened by a new highway;

- Predicted displacement of or loss of homes by families within the community, by demographic group; and

- Job training opportunities and likely jobs created for those within the community, as compared with workforce demographics and jobless rates across geographic locations.

The Department of Transportation must consider these factors in determining whether and how to distribute funds for the project. In other words, consistent with the OMB’s directive on “targeting assistance consistent with other policy goals,” the agency should prioritize support to projects that are likely to promote equal and expanded opportunity, based on both procedural protections and factual evidence.

If, by contrast, those factors indicate that large burdens or benefits will have an unequal impact on the basis of race, gender, ethnicity, or other covered characteristics, the agency must either refuse to fund the project, or determine that an institutional necessity exists and there are no less discriminatory alternatives. If the project has already been funded, and unlawful discrimination comes to light, the Department of Transportation will have to either negotiate project changes to ensure compliance, or terminate funding and possibly seek a return of federal funds.

What Can We Do to Help Protect Equal Opportunity in the Stimulus?

While the OMB Implementing Guidance is clear that agencies must ensure equal opportunity in ARRA- funded projects, there are many steps and agency officials between the White House and the contractors who receive funding to implement the project. It will require the help of active residents and groups in the field to make sure that the federal promise and requirements are actually fulfilled.

Here are a few ways that you can help protect equal opportunity in our economic recovery:

- Educate the Agencies: Federal Agencies have regional offices, each with their own Office for Civil Rights (OCR) that is responsible for enforcing equal opportunity laws. Set up a meeting with your regional OCRs and find out how they are making sure that equal opportunity laws are followed in the projects in your region and state. Remind them that the White House requires not just a speedy economic recovery, but a fair and equitable one that will benefit ALL communities.

- Contact your Elected Officials: Ask your state and local elected officials what they are doing to ensure equitable stimulus spending, and make clear to them what the law requires. Where possible, offer to help them reach communities that have been traditionally excluded from publicly funded projects.

- Find All Your Elected Representatives (requires your 9-digit zip code)

- Let your U.S. Representative and Senators know that oversight of equitable stimulus spending is part of their responsibility, and that any new economic recovery legislation should include strong equal opportunity protections.

- Monitor the Economic Recovery Process: A number of governmental, non-profit, and media websites provide information on where and how ARRA funds are being spent. They include:

In addition, you can observe federally-funded projects in your state or community to see if they are saving and creating jobs that fairly employ community members. A community-based group like a “Recovering Opportunity Committee” can help collect information and share it with job seekers, the media, policymakers, and others.

- Report Violations: Active citizens can directly protect equal opportunity by reporting violations when they occur. The major route for reporting states or contractors who are using ARRA funds in a discriminatory way is to file a complaint with the Agency who issued the funding for the project. If you do not know which Agency is responsible, the Department of Justice’s Office of Coordination and Review can refer you to the correct Agency.

Notes:

* This fact sheet was researched and written on May 21, 2009. The law may have changed. These materials are provided solely for informational purposes and are not legal advice. Transmission of these materials is not intended to create, and receipt does not constitute, an attorney-client relationship. This matter should not be pursued further without contacting an attorney or legal representative.

1. Office of Mgmt. & Budget, Initial Implementing Guidance for the American Recovery and Reinvestment Act of 2009, at p.7, Feb. 18, 2009, as amended by Updated Implementing Guidance for the American Recovery and Reinvestment Act of 2009, at pp.5-6, Apr. 3, 2009.

2. E.g. Title VI of the Civil Rights Act of 1964, 42 U.S.C. § 2000d et seq.; Title VII of the Civil Rights Act of 1964, 42 U.S.C. § 2000e et seq.; Sections 501, 503, and 504 of the Rehabilitation Act of 1973, codified at 29 U.S.C.A. §§ 791, 793, and 794; Title IX of the Education Act, 20 U.S.C. §§ 1681-88; Age Discrimination in Employment Act, 29 U.S.C. § 621, as amended (1967); Americans with Disability Act, 42 U.S.C. §§ 12101-12213, as amended (1990); Fair Housing Act of 1968, Civil Rights Act of 1968, 42 U.S.C. § 3601 et seq., as amended; Fair Credit Reporting Act, 15 U.S.C. § 1681 (1996); Uniform Relocation Assistance and Real Property Acquisition Policies for Federal and Federally Assisted Programs, 42 U.S.C. § 4600 et seq. (1970).

3. Pub. L. 91-190, 42 U.S.C. 4321-4347, Jan. 1, 1970, as amended by Pub. L. 94-52, July 3, 1975, Pub. L. 94-83, August 9, 1975, and Pub. L. 97-258, § 4(b), Sept. 13, 1982.

4. 16 U.S.C. 1531-1544, 87 Stat. 884, as amended (1973).

5. 16 U.S.C. 470 et seq., as amended (1966).

6. Pub. L. 74-403, 946 Stat. 1494, Aug. 30, 1935, as amended by Pub. L. 76-633, June 15, 1940, and Pub. L. 88-349,July 2, 1964.

7. Id. at 4.

8. Id at 5.

9. Id.

10. Id.

11. Id. at 4.

12. Id at 5-6.

13. Id.

14. Id. at 6.